In our previous note, we discussed why we thought that a drug with orphan status, fast-track that tackles metastatic disease would receive a 6-month priority review. However, the FDA didn’t think Chemosat was elegible to get it and granted a 10 month review with a PDUFA date on June 15, 2013. The agency will convene an advisory committee prior to that date. In this article, we’ll try to shed some light on why we think the FDA might have decided not to speed up Chemosat’s review and will analyze the drug’s commercial prospects including a rough Net Present Value calculation.

In short, Chemosat is a drug/device system that isolates the liver in order to administer a high dose of a chemotherapeutic drug. It filters the blood and returns it to the body hence avoiding systemic exposure to high doses of the drug and potential toxicities. Chemosat is considered a drug by the FDA and a medical device by the EMA. Therefore, Delcath must follow the regular drug application process in America by submitting an NDA for review. At the end of 2010 Delcath gathered information on Chemosat and submitted the NDA on a rolling basis. A rolling NDA submission allows companies to send different modules of the NDA at different times up to completion of the total submission. In February 2011, the FDA informed the company that it had refused to file the NDA citing concerns on “manufacturing plant inspection timing, product and sterilization validations and additional safety information, as well as additional statistical analysis clarification” as per the company’s press release on Feb 22, 2011. RTFs are being more and more usual, even for experienced companies. Most RTFs are due to deficiencies in clinical data or CMC. Resubmission timelines depend on the information missing, but it’s unusual for a company to take that much time to resubmit a refused NDA.

The FDA states on its guidelines, that priority review “is given to drugs that offer major advances in treatment, or provide a treatment where no adequate therapy exists”. These advances are, for example:

- evidence of increased effectiveness in treatment, prevention, or diagnosis of disease;

- elimination or substantial reduction of a treatment-limiting drug reaction;

- documented enhancement of patient willingness or ability to take the drug according to the required schedule and dose; or

- evidence of safety and effectiveness in a new subpopulation, such as children.

We can deduct that the FDA has not considered Chemosat worthy of a speed review since it does not provide some of the above requirements. In order to explore the reasons, we will analyze the following aspects:

Clinical data

Let’s take a look at the clinical data from the Phase III trial (NCT00324727) of Chemosat-melphalan in 93 patients with metastatic melanoma to the liver, vs best alternative care (BAC)[1]. Almost 90% of them had ocular melanoma and the rest had cutaneous melanoma. Trial endpoints were agreed upon with the FDA under a Special Protocol Assessment. The primary endpoint was hepatic progression free survival (hPFS) and secondary endpoints were response rate, duration of response and overall survival (OS).

In addition to the results presented at ASCO 2010, updated data presented at the European Multidisciplinary Cancer Congress in Stockholm in March 2011 highlighted the following results:

– hPFS of 8 months vs 1.6 months in the BAC arm. (p<0.0001, HR=0.35).

– Median overall PFS 6.7 months in chemosaturation arm vs 1.6 months in BAC carm (HR 0.36, p<0.0001)

– No difference in OS between arms due to crossover. Median OS in the Chemosat arm was 11.4 months, vs 4.1 months for those patients in the BAC arm that did not cross over.

– Hepatic RR was 34.1% compared to 2% for the BAC arm and 22.2% for patients who crossed-over to receive PHP upon progression of their tumors.

– Stable disease of 52.3% for patients in the Chemosat arm compared with 26.5% in the BAC group, and 40.7% in the crossover group.

Survival

Whereas melphalan administered via the Chemosat system hit the primary endpoint of hepatic progression free survival (hPFS) and response rate, the overall survival was difficult to assess given the fact that patients in the BAC arm were allowed to crossover to the melphalan arm. There were three deaths in the melphalan treatment group, two of them as a result of the treatment and another one due to the stage of disease (unrelated to treatment). According to the company, the safety profile, including those deaths, were in line with that of melphalan.

The crossover design has confounded the survival data so it’s unclear whether Chemosat actually provides a survival benefit to patients compared with the BAC. However, the trial was carried out under an SPA and management has stated the FDA agreed to the crossover. Moreover, removing the patients that crossed over, results in a survival benefit and survival was a secondary endpoint. Although the FDA may have changed its view since the SPA was granted in 2006, and may now require additional survival data.

Changes in the CMC module, the new Generation 2 filter.

Another point of discussion with the FDA may be the inclusion of the Generation 2 filter (Gen2) that has a higher efficiency of 98% compared with Gen1 which is around 80%. This type of filter is being used at least in one center in the EU and has been included in the NDA as part of the CMC module. Since the filtering system is an important safety feature of the system, we think that the FDA may want to see some more data.

Uveal (ocular) melanoma and cutaneous (skin) melanoma.

As we’ve mentioned before, most patients had liver metastasis from uveal melanoma. The incidence of uveal melanoma is 5.3-10.9 cases/million people/year[2]. Median survival for patients with a hepatic metastasis is 6 months with an estimated survival of 15–20% at 1 year and 10% at 2 years, irrespective of treatment. Metastases affect approximately 50% of people suffering ocular melanoma and the liver is the site of almost 90% of all ocular melanoma metastases.

In skin melanoma, liver metastases are common in patients with stage IV melanoma. There’s a probability between 54% and 77% that stage IV melanoma metastasizes to the liver. Metastatic melanoma accounts for 4% of all diagnosed patients. According to SEER, 76,250 new cases of skin melanoma will be diagnosed in 2012[3], that’s 3,050 cases of metastatic melanoma in the US (similar numbers in Europe).

Delcath has included both cutaneous and uveal melanoma in the NDA package, so we see it likely that should this product be approved, it’ll receive a label restricted to uveal melanoma. However, it could be possible that clinicians use it off-label in patients with liver metastases from a number of malignancies, mostly in Europe, but also in the US, depending on the expected clinical benefit and data in hand.

Current treatments.

Patients with liver metastases from primary tumors (mainly metastatic colorectal cancer and met melanoma) amenable for resection, are treated with surgery, which is also the gold standard for hepatocellular carcinoma in non-cirrhotic patients. Unfortunately, most patients are not eligible for surgery and those with unresectable tumors must be treated with other options. If the lesions have spread to many locations in the liver and are small other treatments such as radio and chemoembolization, radiofrequency ablation, systemic therapy, etc. The array of treatments is wide, and some of them are cheaper than Delcath’s method. Other techniques such as Isolated Hepatic Perfusion (IHP), has been used for over four decades, however, associated morbidities and lack of clear efficacy have limited its use. IHP is cumbersome and Chemosat has the advantage of being administered percutaneously, instead of the open surgery required for IHP.

Is there a market for Chemosat?

In recent presentations, management has pictured a multi-billion market opportunity for Chemosat, mainly based on epidemiological data of cancer metastatic to the liver and primary liver cancer in the world’s largest markets. On its last conference call, Delcath reported sales in Europe of $98,000, that amount to the $106,000 previously reported in the second quarter, where the drug device is approved with a broad label. However, only 6 centers are actively using it.

We think that while the commercial potential could in fact be that big, the actual market uptake and use of the system will be much smaller until other applications are approved and the company secures reimbursement in more countries. Delcath’s system is an improvement over other methods that isolate the liver to administer high doses of chemotherapy, but it requires a multidisciplinary group of specialists and is thus relatively costly which hampers its use in broader patient populations. Moreover, it’d be used beyond second line therapy after surgery and radiofrequency and/or systemic therapy.

How big is the market opportunity?

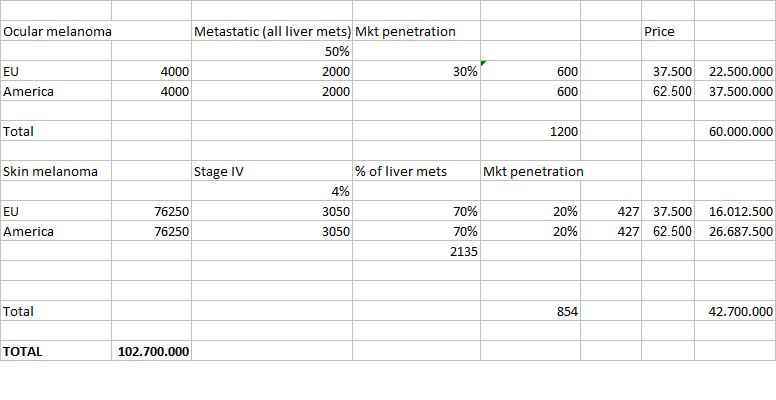

Focusing exclusively on ocular melanoma, with an incidence of 4,000 cases/year in the US and another 4,000 cases in Europe, with half of them being metastatic and assuming all of them are liver mets, this is a potential of 2,000 treatments/year. Assuming a high market penetration of 30% and a price per patient of $37,500 in the EU and $62,500 in America as management has stated[4], that’s $60M revenues in the US and Europe.

If we include cutaneous melanoma, using the incidence figures previously presented, with a penetration of 20% as there are more therapeutic options for stage IV melanoma, and approximately 854 patients treated, that’d amount to $42.7M in the US and Europe.

Delcath does show the potential market for the labeled indications in its presentations. Besides, they add hepatocellular carcinoma, metastatic colorectal cancer and neuroendocrine tumors (NET) to their market calculations. Nonetheless, the company is still far from having Chemosat approved for these indications[5]. They plan to initiate Phase II studies in patients with HCC and mCRC in the first half of 2013. Delcath has recently reported that it received the CE mark for the use of Chemosat with doxorubicin and approval of Gen2 in Australia. Other regulatory approvals are expected or pending for Gen2 in Canada, Hong Kong and South Korea by this year’s end. We are aware that the company has expressed its intention to submit regulatory applications in other areas, with a focus in Asia and South America, but we consider it’s closer to reality to take those areas where the device is approved and/or closer to the market. Moreover, a partnership and some small clinical trials are needed to get the product approved in China, Japan and South Korea. As management hinted in the last conference call, approval in the US could greatly condition a partnership in China and South Korea. In China, the company is looking to treat HCC with doxorubicin (melphalan is not approved in the country) as melanoma has a much lower incidence in the Asian region overall. Australia and New Zealand represent a larger commercial opportunity, however, they do not have any distribution agreement signed yet in this region.

How much is Delcath worth at present?

We made a very rough valuation of the company and arrived at an NPV of $138M, excluding mCRC, NET and HCC and focusing only the European and American markets. We assume a market penetration of 30% in ocular melanoma and 20% in cutaneous melanoma and use a discount rate of 20%. We assume patent expiration in 2016 plus three years exclusivity. All assumptions and data are shown on Table 1. According to this valuation, Delcath’s stock would be fully valued at its current price. We see however a lot more upside in the additional indications the company wants to pursue, but they’d add little value to the current price as they have to go through registrational clinical trials that have the inherent risks and costs of drug development.

Conclusions

One should consider Chemosat as a method for disease management in the liver and a means to improve the patient’s quality of life and clinical parameters related to response and progression free survival. As metastatic ocular and skin melanoma probably has spread to other organs, systemic treatments could be considered in combination with other alternatives previously mentioned. Delcath has not disclosed how many patients in the Phase III trial had liver-only metastases and how many had mets to other organs. Although the device is approved in Europe with a broad label, clinical data so far support its use mainly in ocular melanoma and we think that physicians will want to have more evidence in other indications before start using this therapy in those settings.

Commercial concerns linger over Delcath. The product is generating few revenues in Europe and the company is struggling to get reimbursement for the product. It’s recently gotten it in Italy and has filed for it in Germany and the UK. Getting the product approved and marketed in the US needs to pass the scrutiny of the FDA and an advisory committee. In the rest of the world, sales may come in Australia and New Zealand some time in 2013 with the unknown of the Asian region until there’s more clarity on partnerships which will catalyze the process in the continent.

Delcath reported on its Q3 conference call that it has cash and cash equivalents of $28.3M with a burn rate of approximately $14M per quarter. The company replaced its December 2011 shelf by filing a new Form S-3 shelf registration that became effective on October 9 to raise up to $100M through the sell of stock, warrants and debt securities. Delcath also has $24.5M available under its ATM program. We suspect the company will announce an offering rather sooner than later, probably by the end of the year.

Our valuation of the stock shows a net present value of $138M or a price per share of $2.06. We think it’s a generous valuation given the limited commercial prospects of its main product.

Disclosure: no positions.

[1] decided by the patient’s treatment team and could involve interleukin 2, ipilimumab, transcatheter arterial chemoembolisation (TACE), systemic chemotherapy or inclusion in a clinical trial

[2] http://www.hindawi.com/journals/jsc/2011/573974/

[3] http://seer.cancer.gov/statfacts/html/melan.html

[4] Price/treatment: EU $15k and US $25k. Company assumes 2.5 treatments per patient

[5] Delcath has tested Chemosat in small cohorts in all three diseases. The mCRC cohort didn’t show efficacy due to advanced disease status. Good signs of efficacy were seen in HCC and mNET.

{kind=link}